Q3 2025

Dear Investors and Colleagues,

We are pleased to share with you our latest issue of Perspectives from the Lighthouse, our quarterly newsletter featuring our insights on the past quarter and updates from across the fund. The third quarter of 2025 marked a transition from uncertainty to renewed confidence, driven by major regulatory milestones, the Fed’s first rate cut of the year, and growing institutional participation in digital assets. Despite ongoing geopolitical pressures, the market showed resilience and maturity, setting the stage for a constructive close to the year.

Executive Summary

Q3 2025 marked a significant turning point for the crypto market, particularly in the United States, as the industry navigated persistent macroeconomic headwinds and a complex geopolitical landscape. This quarter was defined by a shift from regulatory uncertainty to a new era of clarity, driven by landmark legislative and policy developments. The crypto market not only absorbed volatility but also matured, attracting deeper institutional capital and strengthening its position as a legitimate asset class. The overall crypto market capitalization reached a robust $4.11 trillion, with Bitcoin and Ethereum proving particularly resilient. The market's ability to "climb a wall of worry," looking past near-term challenges and positioning for future growth, was a key theme.

Geopolitical and Macro Commentary

Q3 began with the lingering effects of Q2's "wall of worry," characterized by the US-led global tariff war and lingering geopolitical tensions. However, the narrative shifted from a defensive, risk-off stance to one of cautious optimism as markets proved resilient.

The Unraveling of Trust: Tariffs, the Dollar, and the Rise of Gold:

President Trump's sweeping tariff policies, which took effect in August, have created significant market volatility and undermined trust in the US dollar as a global benchmark. The erratic nature of these policies has made the US dollar and its assets less reliable, pushing international investors to diversify away from the greenback. A lack of clarity on which goods would be tariffed and when the levies would be implemented created widespread confusion among businesses and financial markets. This policy unpredictability is considered even more problematic than the tariffs themselves. This dynamic has had a notable impact on the bond market, particularly on the long end of the yield curve. Following the tariff announcements, investors sold off both U.S. stocks and Treasury bonds. The 30-year yield, for example, climbed by about 40 basis points after the April 2 tariff announcement, a sharp contrast to previous periods of economic uncertainty when investors would have flocked to long-term bonds. The selloff of Treasury bonds contributed to a weakening of the US dollar against other major currencies, a trend that began in April and continued through to the end of Q3. This dynamic has provided a major boost to safe-haven assets. The price of gold, in particular, has benefited from the turmoil, with a strong negative correlation to the US dollar. Gold has rallied by more than 50% this year, setting a record above $4,000 an ounce on October 8th. The price has been further supported by central banks diversifying their reserves away from traditional currencies, a trend that has accelerated since 2022.

Will Bitcoin participate in gold’s rally: Bitcoin has emerged as a complementary asset to gold in this environment, with both setting new all-time highs amid rising global uncertainty. Its appeal as a geopolitical hedge is growing due to its decentralized nature, scarce supply, and low correlation with other asset classes. The ongoing US government shutdown and policy uncertainties have further fueled demand for Bitcoin, as investors seek to protect their assets from political crises. A Deutsche Bank Research Institute report predicts that Bitcoin will join gold in many central banks' official reserve balance sheets by 2030.

Federal Reserve and US Macroeconomic Policy

The Federal Reserve's journey through Q3 2025 was marked by a decisive shift in its policy trajectory, driven by a weakening labor market despite some lingering inflation concerns. This pivot culminated in the first rate cut of the year in September.

Easing vs. Risk Management:

The Fed’s 25-basis-point cut in September was widely expected by markets, but Fed Chair Jerome Powell was careful to frame it as a "risk management cut" rather than the start of a deep easing cycle. This distinction is critical: a pure easing cycle is meant to stimulate an economy, while a risk management cut is a proactive move to guard against potential, but not yet realized, economic downturns. Powell’s comments were aimed at threading the needle between addressing signs of a cooling labor market and acknowledging the ongoing, albeit contained, inflationary risks.

The Tug-of-War: PPI vs. CPI and a Weakening Jobs Market:

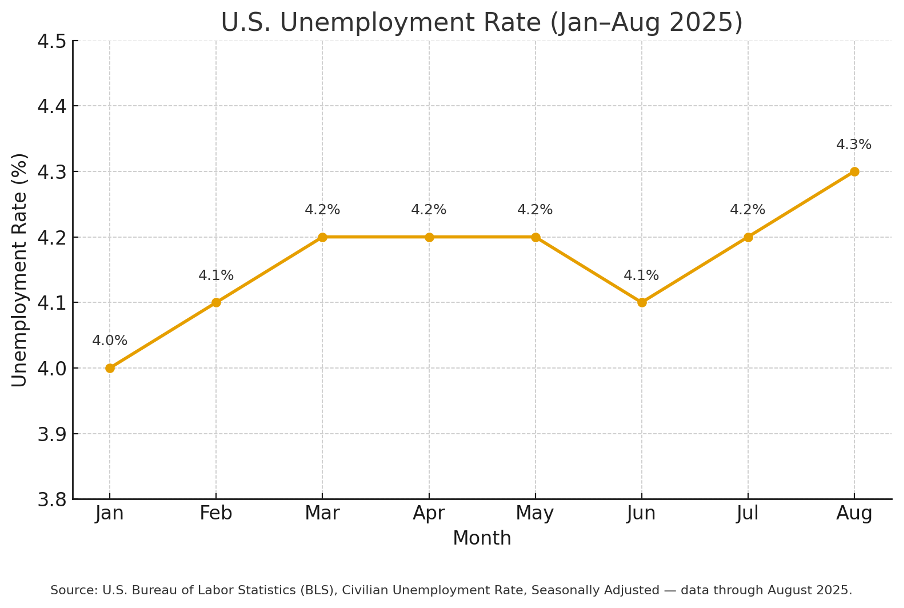

Early in the quarter, the Fed faced a mixed economic picture. The July Producer Price Index (PPI) surged by 0.9% month-over-month, its largest increase in over three years. This outpaced economists' forecasts and was seen as a clear sign that President Trump's tariffs were beginning to drive up the cost of imported goods. While the PPI measures prices from the producers' perspective, it is often seen as a leading indicator of what's to come for the Consumer Price Index (CPI), which tracks prices for consumers. The July CPI report, released two days prior, was cooler than expected. This created a dilemma for the Fed: a cooler CPI report made a rate cut seem more likely, but the rising PPI data hinted at future inflationary pressures, making a rate cut more difficult. However, the inflation fears from the PPI report were eventually outweighed by mounting evidence of a weakening labor market. An ADP report showed job cuts in September and revised August employment down, while Treasury yields fell. The Bureau of Labor Statistics (BLS) also revised its payroll employment growth figures lower by a much larger than expected 911,000 for the 12 months ending in March 2025.

Volatile Environment and Political Pressure:

Amid this economic uncertainty, the Fed’s independence was repeatedly called into question by the Trump administration. President Trump continued to push for aggressive rate cuts, publicly stating that the Fed should "listen to smart people, like me". This political interference created volatility and raised concerns among investment experts about the long-term credibility of government data and the stability of US markets.

Powell's "One-Time" Inflation and the September Rate Cut:

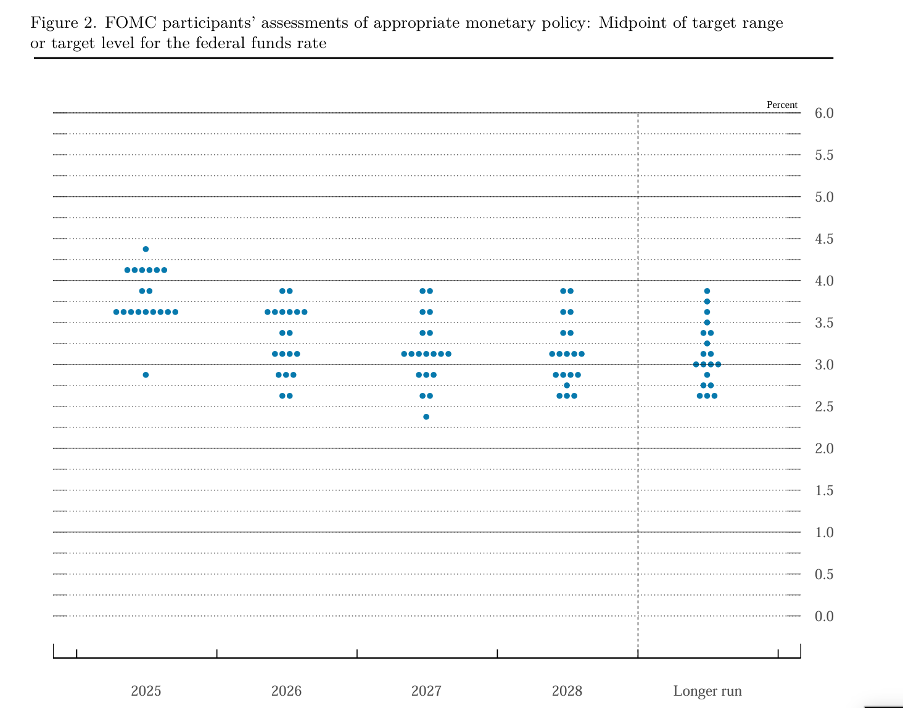

Despite the tariff-driven PPI increase, Fed Chair Jerome Powell maintained his long-held view on the nature of this inflation. He said that while the effects of tariffs on consumer prices are now "clearly visible," a "reasonable base case is that the effects will be relatively short lived—a one-time shift in the price level". He further clarified, "Of course, 'one-time' does not mean 'all at once.' It will continue to take time for tariff increases to work their way through supply chains and distribution networks". This philosophy provided the Fed with cover to ease policy in the face of persistent price pressures, as they believe the underlying inflation risk is contained. The culmination of these factors was the Federal Open Market Committee (FOMC) meeting on September 17, 2025, where the Fed delivered a 25-basis-point interest rate cut, bringing the federal funds rate to a range of 4.0%-4.25%. The Fed's new posture was formalized in its September dot plot, which revealed a more aggressive cutting cycle than previously projected. The median of Fed members now expects the fed funds rate to fall to a range of 3.5%-3.75% by the end of 2025, implying two more cuts of 25 basis points at the remaining two meetings of the year. The distribution of views among the 19 FOMC participants remains wide and "fairly bifurcated".

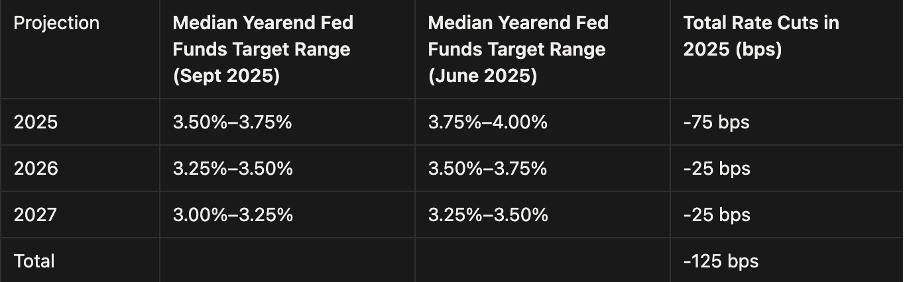

Summary of Fed Dot Plot Projections (September 2025 vs. June 2025)

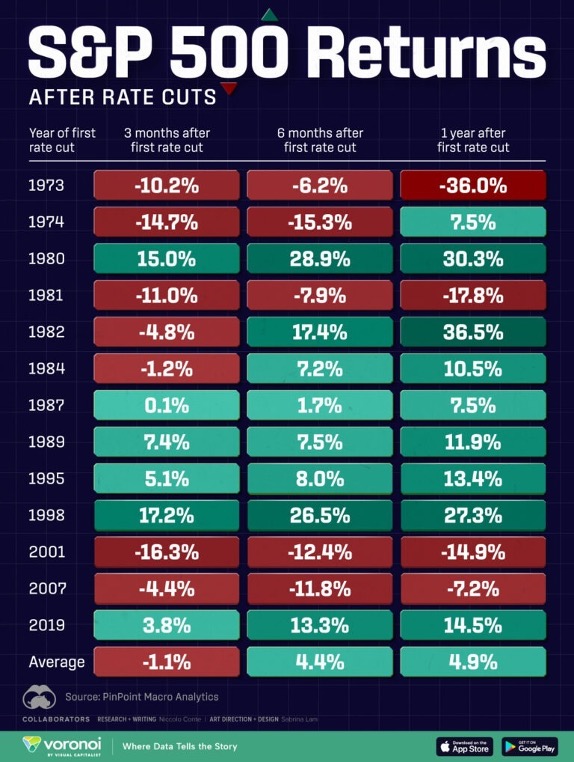

Historically, the S&P 500's performance after the start of a rate cut cycle has been mixed but generally positive. Since 1973, the S&P 500 has returned an average of 4.9% one year after the first rate cut. Markets tend to decline in the first three months after a cut but typically rebound six months later.

Digital Asset Treasury Proliferation and Potential Risks

The third quarter saw a decisive turning point in the corporate adoption of digital assets. Once seen as a speculative play, digital asset treasuries (DATs) are now a strategic component of corporate finance, used for diversification and risk management. The total market capitalization of DATs has increased more than threefold to approximately $150 billion in September 2025, compared to $40 billion in September 2024. The proliferation of DATs has fundamentally shifted market dynamics, with public companies in the US, Asia, and Europe now collectively holding $109.49 billion in Bitcoin and over $17.6 billion in Ethereum across 19 major firms.

Pioneers and New Entrants:

- Strategy (formerly MicroStrategy) continued to lead the charge, with its Bitcoin holdings exceeding 640,000 BTC by the end of the quarter, representing almost 72% of all corporate Bitcoin treasury holdings. The company reported an impressive $3.9 billion in Bitcoin value appreciation in Q3.

- Metaplanet, a Japanese company, became the fourth-largest corporate Bitcoin holder globally, surpassing its 2025 target ahead of schedule with total holdings of 30,823 BTC.

- BitMine Immersion (BMNR) emerged as a major player, holding over 2.83 million ETH tokens and reigning as the largest ETH treasury in the world, and the #2 global treasury behind Strategy.

The Ticking Time Bomb: Leveraged Treasuries and Insolvency Risk: While the adoption of DATs appears bullish, the underlying financing models for many of these new entrants, particularly those using leverage, present a significant risk. The use of debt, often in the form of convertible notes or perpetual preferred shares, to acquire volatile digital assets creates a "ticking time bomb". This strategy works as long as asset prices are rising, but if there is a significant drawdown, the model can quickly reveal its cracks. A 20% drop in Bitcoin's price could result in a 40% or greater hit to shareholder equity for a leveraged firm.

- Funding Gaps and Liquidation: Many of these new digital asset companies have weak or stagnant core operations and are using Bitcoin to "reinvent themselves". The cash flow from their businesses is often insufficient to cover the dividend obligations on their debt. If new investors stop buying the preferred shares, the company faces an immediate stress event and could be forced to liquidate its digital asset holdings into a declining market to cover its obligations.

- Systemic Risk: This creates a procyclical and systemic risk. As asset prices fall, these leveraged companies are forced to sell, adding to the downward momentum and creating a "domino effect" of forced liquidations across the market. We have seen this "movie before" with past collapses like Celsius and Three Arrows Capital, where excessive leverage led to a brutal unwind and widespread sell-offs.

The Rise of Private Blockchains: A New Threat to Public L1s?

Q3 saw major players in traditional finance and fintech begin to launch or develop their own private or permissioned blockchains, posing a new strategic challenge to established public Layer-1 (L1) chains like Ethereum and Solana.

Circle's Arc: Circle announced the launch of Arc, an open Layer-1 blockchain built specifically for stablecoin finance. Unlike general-purpose blockchains, Arc is purpose-built to deliver enterprise-grade performance and regulatory alignment. It addresses key pain points for enterprises on public chains, such as unpredictable fees (by using USDC as its native gas token), the need to hold volatile crypto for transactions, and a lack of data privacy. Arc offers opt-in privacy controls, allowing businesses to shield sensitive data while remaining compliant with regulators.

Google and Robinhood: This trend is not limited to Circle. Robinhood is developing its own Layer-2 blockchain, optimized for tokenized real-world assets like stocks and ETFs, aiming for 24/7 trading and seamless bridging. Similarly, Google Cloud has partnered with the CME Group to pilot a private, permissioned distributed ledger called the "Universal Ledger".

Implications for Ethereum and Solana: The rise of these private blockchains is a double-edged sword for public L1s. While it validates the core technology, it also represents a potential shift in institutional and corporate activity away from public, permissionless networks. The ultimate outcome will likely be a hybrid approach, with private and public chains co-existing and interoperating to serve different needs, the question remains what impact the competition from private Layer-1’s will have on Ethereum, Solana and other prominent public Layer-1’s

US Regulatory and Policy Developments

The most impactful events of Q3 were not market-based, but political. The US saw unprecedented momentum toward a clear regulatory framework, which is now a major tailwind for the market.

The GENIUS Act Becomes Law: The Guaranteed Electronic Notes, Issuers & Unitary Stablecoins (GENIUS) Act was a landmark achievement. As discussed in our Q2 2025 newsletter, the Act establishes a federal charter for payment stablecoin issuers, mandating 1:1 reserves with cash or cash-equivalents, and imposing strict AML/KYC requirements. This bill is the clearest signal to date from Washington that it supports the sector, viewing stablecoins as a "force multiplier of our economic might" rather than a threat to the US dollar.

The CLARITY Act and SEC/CFTC Harmony: The House passed the Digital Asset Market Clarity (CLARITY) Act, which aims to provide regulatory clarity by distinguishing between digital commodities and securities. It would grant the CFTC exclusive jurisdiction over digital commodities and their spot markets. This legislative push was mirrored by a landmark Joint Statement from the SEC and CFTC on September 2, 2025. The agencies clarified that registered exchanges are not prohibited from listing certain spot crypto products, effectively ending years of regulatory ambiguity and signaling a new era of cooperation.

SEC's Innovation Exemption: In a significant policy shift, new SEC Chair Paul Atkins has announced a new initiative called "Project Crypto," launched in July 2025. A key component of this project is the planned "innovation exemption," a temporary regulatory relief that will allow digital asset firms to launch products like token sales, staking, and multi-asset trading with reduced compliance burdens. The exemption is a "regulatory carve-out" from older, more rigid securities rules. Atkins has argued that very few tokens are actually securities, a direct departure from Gensler's view.

The Rise of Perpetual Futures in the US Market

Q3 was a transformative quarter for US traders, as a key segment of the global crypto market—perpetual futures—finally became legally accessible domestically. For years, US traders were largely relegated to a handful of domestic exchanges with fewer options and poor liquidity, while international counterparts traded on deep global liquidity pools. Perpetual futures, or "perps," which allow traders to speculate on an asset's price without an expiration date, dominate the global crypto derivatives market, accounting for an estimated 59% of all derivatives activity. The total trading volume of perpetual futures reached an estimated $12 trillion in Q2 2025, with over $100 billion traded daily.

CFTC Reopens Access to Offshore Exchanges: In a landmark advisory on August 28, 2025, the Commodity Futures Trading Commission (CFTC) reaffirmed its Foreign Board of Trade (FBOT) registration framework. This move provides a clear legal pathway for non-US exchanges to serve American traders. While US retail investors still cannot access these exchanges directly, the advisory allows professional US traders to legally access these platforms through intermediaries. Acting CFTC Chair Caroline D. Pham stated that the advisory provides "regulatory clarity needed to legally onshore trading activity that was driven out of the United States" due to past "regulation by enforcement".

Coinbase Launches US Perpetual-Style Futures: In parallel, Coinbase took a significant step by launching the first US-regulated "perpetual-style" futures in July. These new contracts for Bitcoin and Ether are designed to replicate the functionality of international perpetuals, including a funding rate mechanism to keep prices aligned with the spot market and offering up to 10x leverage. This product suite is the "first of its kind in the US, filling a critical gap in the domestic derivatives market".

Importance of Perpetual Futures: The debut of perps in the US is a game-changer for several reasons. The funding rate mechanism of perps is crucial, as it incentivizes traders to enter positions that correct price discrepancies between the futures and spot markets, promoting market efficiency and price discovery. Perps also offer capital efficiency and leverage, allowing traders to amplify their exposure with smaller capital. This also makes them a valuable tool for hedging, enabling long-term investors to protect their portfolios against sudden downturns without selling their core holdings.

Q3 IPOs and the Future of Crypto Public Markets

Q3 saw a significant number of IPOs, with the US market being particularly strong. The US had 180 IPOs in the first three quarters of 2025, raising $33 billion, a significant increase from 121 IPOs and $27.3 billion in the same period of 2024. A number of key crypto and fintech companies went public, signaling a major turning point in the industry's integration with traditional financial markets.

Circle and Gemini Lead the Charge:

Following the success of prior listings like Bullish, the stablecoin issuer Circle (CRCL) and the crypto exchange Gemini (GEMI) both went public in Q3 2025. Circle’s IPO was highly anticipated and proved to be a resounding success, with its stock price skyrocketing from its $31 per share IPO price to close at $82.84 on its first day of trading, a 167% jump. The strong demand for Circle’s stock indicates that investors are increasingly seeing the value of stablecoin integrations with traditional finance. Gemini also had a successful IPO, with the Nasdaq exchange itself buying a stake as a strategic investor, lending significant industry validation to the crypto exchange. The success of these Q3 IPOs bodes well for the future. Several high-profile firms, including the crypto exchange Kraken and asset manager Grayscale, are rumored to be preparing for public offerings. A number of other companies, including lending and infrastructure provider Figure Technologies and custody service BitGo, are also expected to go public once regulatory clarity firms up. The successful IPOs of Circle and Gemini have laid the groundwork for a continued appetite for public crypto investments, reinforcing the notion that crypto finance is moving into the mainstream.

Forward-Looking Commentary: The Outlook for Q4

Q4 is set to be a transformative period, building on the regulatory and institutional momentum of Q3. The market is now positioned for significant upside, although a few key risks remain.

The Crypto Halving Cycle: Bitcoin's market cycles have historically followed a predictable four-year rhythm, anchored by the halving events that cut the new supply of Bitcoin in half. The last halving occurred in April 2024. Based on historical patterns, a major bull run typically starts 6-12 months after the halving, with the peak occurring 500-550 days later. As of late September 2025, Bitcoin is in the later stages of its "uptrend" phase, roughly 520 days after the halving. Given this, analysts are projecting a potential cycle peak sometime between late September and mid-November 2025. However, some analysts are skeptical that the four-year cycle will remain as relevant as it once was due to the increasing institutional adoption of the asset.

The CLARITY Act: The biggest event on the horizon is the potential passage of the CLARITY Act in the Senate. The bill would officially clarify regulatory oversight and provide a much-needed framework for the industry, potentially unlocking significant sidelined capital.

Fed Policy and Rate Cuts: With the Federal Reserve signaling further rate cuts, crypto assets are expected to benefit. A decisive Fed pivot or trade agreements could restore investor confidence and unlock capital. The Fed will be watching closely for whether indicators of a weakening labor market worsen.

The Multi-Asset ETF Era: Following the approval of generic listing standards for Grayscale's Ethereum ETFs, a Bloomberg analyst noted that SEC approval odds for spot crypto ETFs are now "essentially 100%". A Solana ETF could be approved any day, signaling a potential expansion of the spot ETF selection into a multi-asset era.

The groundwork laid in Q3 positions the crypto industry for a constructive second half of 2025. With regulatory clarity accelerating, infrastructure maturing, and capital returning, the path forward looks increasingly aligned with integration, adoption, and upside.

Lighthouse Capital is the trading name of Lighthouse Collective Capital Fund Ltd.