Q2 2025

Dear Investors and Colleagues,

We are pleased to share with your our latest issue of ‘Perspectives from the Lighthouse’ our quarterly newsletter featuring our insights on the past quarter and our fund updates as we look ahead. The second quarter of 2025 could be defined by one word: uncertainty. From global trade wars to kinetic wars, capital flows and asset pricing were driven more so by geopolitical tensions, and policy movements rather than market fundamentals.

The Quarter in Review:

April opened Q2 with a jolt as President Trump’s sweeping “Liberation Day” tariffs - a broad set of trade duties targeting allies and adversaries alike. Implemented as a method to reassert American industry power, cut trade deficits, and end the “overseas extortion” of American companies, the aggressive tariffs immediately triggered retaliatory measures from Beijing, including the restriction of rare earth mineral exports, a renewed blacklisting of U.S. tech firms, and export controls on critical chip components. Markets turned extraordinarily risk-off due to the extreme measures laid out by Trump’s tariff policies, with fears of a global economic stand-off and a decoupling of the world’s largest economies gripping participant sentiment. Equities, semiconductors and industrials in particular, faced extremely large drawdowns as the Philadelphia Semiconductor Index saw its worst monthly performance since late 2023. The fear of a global trade war shifted investor focus from fundamentals to volatility, with macroeconomic and geopolitical news puppeteering markets to the utmost extent. This unprecedented fiscal policy set the tone for the rest of the quarter.

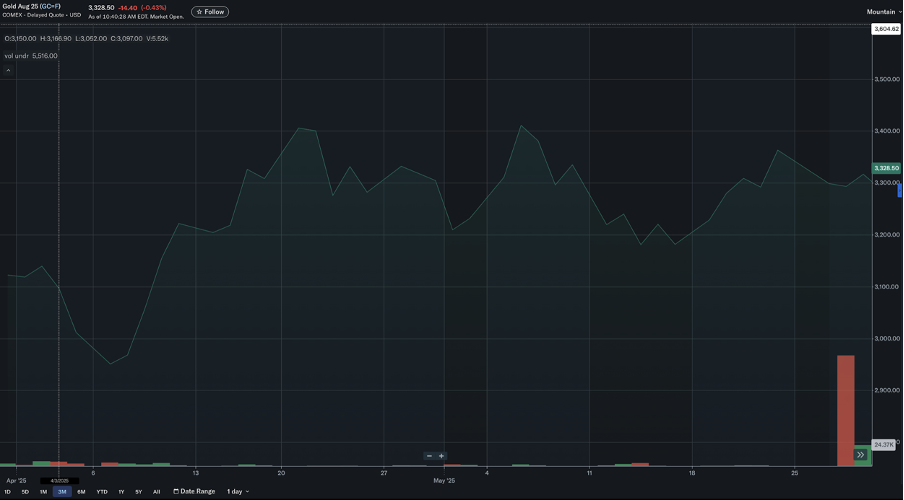

In the weeks that followed, markets responded swiftly and brutally: Treasury yields shot up, risk assets saw large sell-offs, and almost everything went into the red, with the S&P 500 falling just over 10% in the three days following the news. Facing mounting criticism and pressure, the White House implemented a 90-day pause on all ‘reciprocal’ tariffs expect those put in place against China, which were increased to a staggering 125%. However, a brief window of optimism emerged when US and Chinese officials re-entered negotiations after tit-for-tat responses from both nations, categorised by a formal phone call between President Trump and President Xi Jinping. Global markets welcomed the prospect of de-escalation with risk assets staging a short-lived rebound, however, the talks collapsed as both nations blamed the other for a lack of transparency and follow-through on their promises. Due to this, investment sentiment soured once more as the bilateral relationship deteriorated further. By late April / early May, the effects of the failed negotiations were completely priced in, with markets remaining risk-off, and capital flowing out of cyclical sectors and into defensive assets such as gold, which saw a new ATH this quarter, reaching around $3500 for an ounce of bullion:

Yields remained elevated, with the 10-year T-bond pushing toward 4.5%, while short-term rates began flattening in anticipation of the Fed being forced to cut interest rates, despite Powell and his team standing firm in their ‘wait-and-see’ stance. The end of May brought complications to Trump’s foreign policy, with the U.S. Court of International Trade ruled the widespread tariffs unlawful. However, rather than providing clarity, this decision seemingly deepened the complexity of the situation as the White House immediately appealed the allegations, thus igniting a high-stakes Supreme Court battle which is yet to materialise. As of writing, the tariffs are set to remain in place, with the 90-day pause established in April expiring on July 9th now being extended once again to August 1st. This second postponement has markets shifting back into a risk-on sentiment, with the belief that the tariff enforcement may be another ‘TACO’ (Trump Always Chickens Out) trade, thus keeping market tailwind strong despite the looming economic threat.

Early June brought further complications between the U.S and China, with both nations restricting access to materials and software the other needed, further mounting pressures on global manufacturers, foreign policy makers, and private companies. However, a much-needed sliver of relief finally arrived shortly after the aforementioned developments, with two days of talks in London between Treasury Secretary Scott Bessent and China’s vice-premier He Lifeng. Following the lengthy discussions, the two nations announced a framework tariff truce: Washington would reduce China-specific duties to around 55%, while Beijing would trim its retaliation to about 10%, while restarting rare-earth exports under a pilot period of six months. Despite the deal omitting details regarding other pressing tariff-related issues between the two nations, markets bounced upon receiving the news, however, the deal is yet to be formally approved by both President’s, and should it go through, will be implemented in August.

As calm, clarity, and conviction began to reclaim markets in mid-June, another geopolitical shock occurred, when the simmering Iran-Israel conflict burst into active warfare. On June 13th, Israel launched ‘Operation Rising Lion’ a surprise attack on key nuclear and military facilities within Iran, prompting a series of missile exchanges between the two nations. The Israeli operation was a massive success but to complete their objective of removing the Iranian nuclear threat, they required the 30 000 lbs Massive Ordinance Penetrator ‘MOP’ bomb that only the US had the means to deliver. On June 21st we heard about ‘Operation Midnight Hammer’ the US action to ensure total destruction of Iranian uranium enrichment facilities. In the quiet of the night, seven B-2 Spirit bombers dropped 12 MOP’s on their targets at Fordow and 2 more on Natanz, crippling their functional capabilities, in addition the US launched 30 Tomahawks from its Ohio class submarines at the Isfahan conversion facility completely neutralising the threat of an immediate Iranian nuclear weapon. In a diplomatically charged attack, Iran struck the Al Udeid Airforce Base in Qatar (an attack that was given advance warning by Iran. A few hours after the attack, President Trump announced a ceasefire deal reached between Israel and Iran, thus brining an apparent end to the “Twelve Day War”. The conflict brought extreme volatility to equity and crypto markets, while energy and defence out-performed, as seen by the rapid increase in oil, with Brent Crude Oil reaching around $77/bbl.

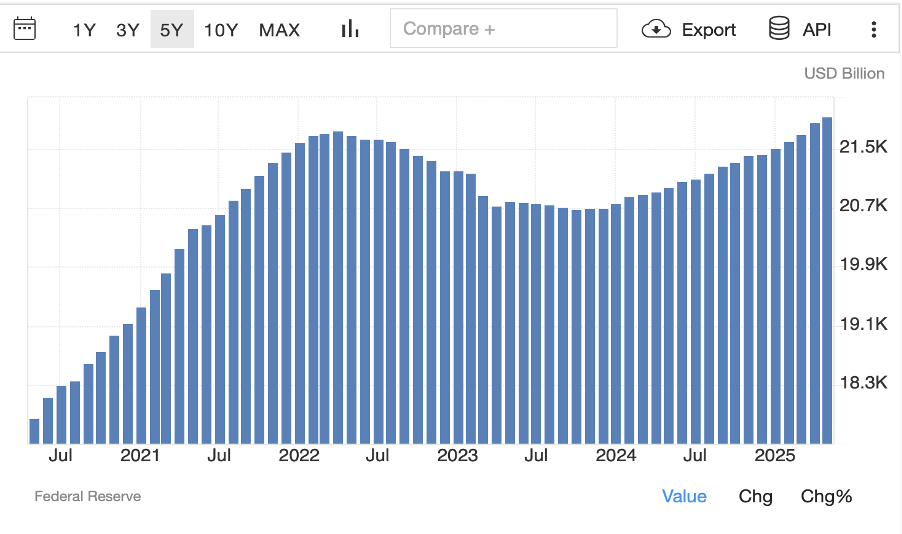

Turning away from foreign policy, monetary policy did not offer a helping hand to the situation. At the FOMC meeting on June 18th, Fed Chair Powell held rates at 4.25-4.50%, citing continued inflationary pressures from the Trump administration’s tariff policies, a tight labour market, and a renewed volatility in energy markets due to geopolitical tensions. Nevertheless, Powell reiterated the Fed’s adoption of a ‘wait-and-see’ stance, citing that any decision regarding rate cuts will be made on a data-driven basis, rather than headline noise. Recent economic data reinforces the Fed’s cautious approach, with the U.S. Core PCE Price Index rising back to 2.7% year-over-year in May, reversing the slight cooling seen in April, with the 0.2% month-on-month rise exceeding expectations, reinforcing the possibility of disinflation stalling rather than reversing, and keeping core inflation above the Fed’s 2% target further complicating their decision making. Treasury yields remained elevated, reflecting the ongoing uncertainty, with the 10-year yield closing the quarter at 4.24%, and the 30-year yield at 4.755% both above their Q1 closes. Despite restrictive monetary policy, the U.S. M2 money supply has continued to climb over this past quarter, with the most recent data available illustrating it sat at $29.1T by the end of May, its highest level since the peak of the COVID-19 pandemic.

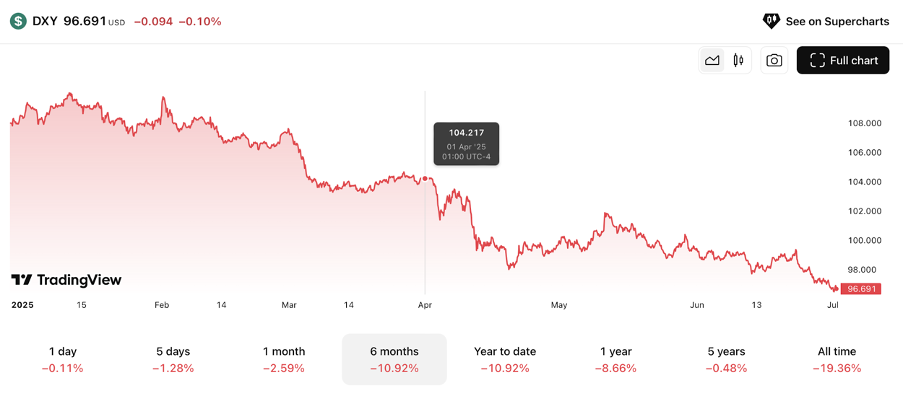

The graph showing M2 money supply above suggests that liquidity is slowly but surely returning into the system regardless of a cautious Fed stance. Simultaneously, USD ($) saw its steepest quarterly decline in years, with the U.S. Dollar Index (DXY) falling over 7% in Q2, closing at its lowest level since the pandemic. This sharp decline over the past few months illustrate growing concerns regarding U.S. fiscal stability, global confidence in the dollar, and the costs of adopting such aggressive foreign policy. Whilst liquidity may be returning, it is occurring in an environment where the dollar’s role as the global benchmark currency is being quietly, but seriously questioned.

Despite the quarter being riddled with geopolitical tensions, unforeseen fiscal policies, and uncertain market conditions, digital assets proved notably resilient. While BTC briefly dipped below $100,000 during the peak of the Iran-Israel conflict it quickly rebounded as continued ETF inflows and dip-buying from large market participants helped to stabilize panic-selling. This remarkable resilience was seen mostly in BTC, with other altcoins receiving heavy sell-offs, however, such a strong performance is promising, with the concept of Bitcoin proving its use case as a hedge against geopolitical uncertainty. As of quarter-end, total crypto market cap sat above $3.43T, up nearly 40% year-on-year, despite ongoing macro volatility challenging most asset classes. BTC dominance rose to 65.3%, reflecting the aforementioned narrative of Bitcoin as a safe, strong asset to hold in the face of uncertainty, while stablecoins total market capitalization ended Q2 at $263B, following the successful passing of the GENIUS Act in the Senate. As Q3 begins BTC has held remarkably strong through a whirlwind of chaos, with current market behavior pointing towards increased institutional adoption, and a more matured asset class which is now beginning to play its part in the global monetary system.

Looking ahead:

As July opens with the cessation of the conflict with Iran, the markets resolved to more of a risk on attitude with the S&P500 reaching an all time high. As the stock markets climb a ‘wall of worry’ tariffs have once become front and center with the Trump administration issuing a flurry of letters to US trading partners ahead of the July 9th deadline. Despite this, the crypto market has followed on the heels of the stock market and as of time of writing, BTC has reached a new ATH of $119,450, ETH has reached $3000, its first time to do so since February buoyed by ETF inflows, and SOL may be next in line for its own ETF. While volatility remained elevated due to the unresolved tariff and interest rate issues markets are trending upward, reflecting confidence in the long-term viability of digital assets, with the most recent data showing the number of transactions on blockchains was at an all-time high by June as evidenced by the chart below:

Overall, the top 3 asset’s ability (BTC, ETH, SOL) to generally remain above support price levels despite extreme volatility seen last quarter showcases the growing support and belief in the digital asset space as not only a macro hedge, but as the next step in the narrative of money.

Altcoins:

With Bitcoin dominance edging +3.11% last quarter (62.25 % → 65.36 %), the long-awaited alt-season was deferred yet again. Nevertheless, this capital rotation reflects a flight to quality amidst macro uncertainty, with investors prioritizing liquidity, narrative strength, and safety within assets, areas where BTC continues to dominate.

The next alt-season will likely depend on one of the following catalysts:

- A clean ETH break-out and sustained dominance rotation: Spot ETH funds are now live, flows remain tiny relative to BTC but are growing steadily.

- Regulatory clarity for DeFi tokens: The U.S. CLARITY bill and the EU’s MiCA Part 2 (December) will decide whether large allocators can touch governance-token revenues.

- Macro risk-on switch: A decisive Fed pivot or trade agreements between the U.S and tariff-induced countries may unlock sidelined capital while restoring investor confidence.

- Broader ETF palette: June’s first Solana spot-ETF filing (plus Bitwise’s DOGE & APT amendments) signals that a multi-asset ETF era is coming; SEC approval would be a game-changer for non-BTC digital assets.

Until one or more of those catalysts land, altcoins are likely to keep lagging the majors, even while other aspects of the space continue to register strong progress and performance.

ETFs:

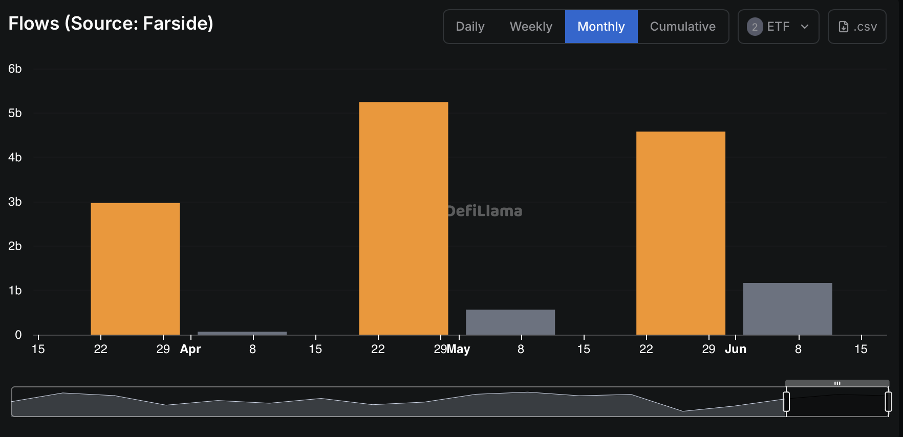

Q2 proved strong for crypto ETFs. Following a volatile April, stemming from macroeconomic uncertainty, BTC ETFs saw a large revival mid-May, with a net monthly inflow of around $5.2B, driven primarily by BlackRock’s IBIT, with Fidelity’s FBTC following suit. The total Q2 net inflows for BTC spot ETFs reached around $12.3B. Meanwhile, ETH ETFs saw their first real movements this year, following a relatively quiet Q1, netting total inflows of around $1.8B in this quarter, up from around $120M in the previous quarter. These numbers showcase an increased institutional interest in ETH, while reinforcing BTC’s role as the institutional backbone of the digital asset space. June was particularly active despite geopolitical tensions, with around $4.58B being added into BTC ETFs. The continued demand for IBIT and FBTC - the two largest spot BTC ETFs - showcase their resilience even amidst geopolitical volatility and general uncertainty. At the end of Q2, IBIT closed with just under $75B AUM, maintaining dominance over the ETF market, and further deepening institutional trust in the digital asset class.

ETF product innovation also continues to evolve, with the first major filing for a spot Solana ETF filed on June 30th. This marks a big step forward in crypto ETFs, and pushed the SEC to address its regulatory stance towards alternative L1s beyond BTC and ETH. In addition, Bitwise also updated their filings for DOGE and APT ETFs to include in-kind redemptions, thus signalling a potential expansion of the spot ETF selection heading into the second half of the year.

Overall, Q2 reinforced spot crypto ETFs as structural allocation tools for institutional capital, rather than speculative gateways into the world of digital assets. With total inflows amounting to slightly under $15B this quarter, ETFs continue to provide a liquid, regulatory compliant entry point for institutional capital. The continuously improving infrastructure alongside increased product diversity, line Q3 up for the beginning of a multi-asset ETF era, further growing the legitimacy of crypto as a core portfolio allocation.

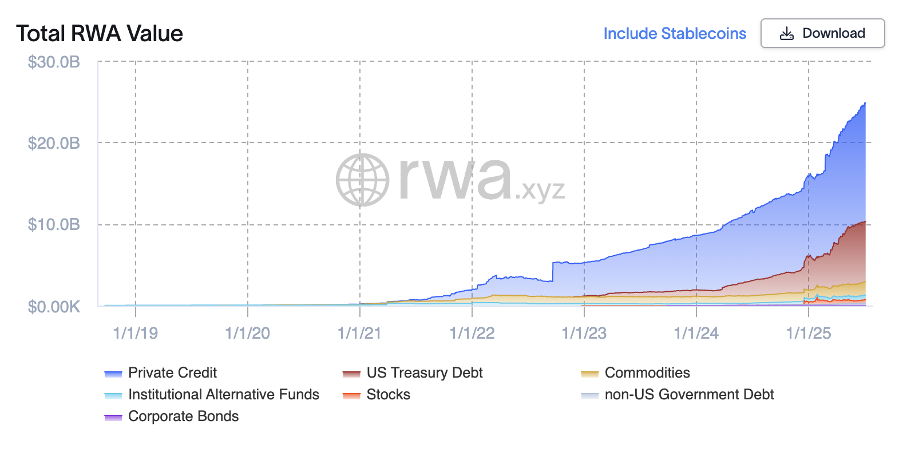

Tokenisation of RWAs:

The tokenisation of real-world assets (RWAs) has emerged as a defining theme in the convergence of TradFi and blockchain infrastructure. As major institutions seek efficiency, transparency, and broader market access, the shift toward on-chain representations of assets such as treasuries, private credit, and real estate is accelerating. Unlike assets which are crypto-native, tokenised RWAs bring off-chain value on-chain, allowing these instruments to be traded 24/7, used as DeFi collateral, and settled faster through the use of smart contracts. This injects real-world liquidity into blockchain finance, while opening up new capital efficiency methods for market participants.

Throughout Q2, the tokenisation ofRWAs gained meaningful, tangible progress. Blackrock’s Ethereum-based BUIDL fund surpassed $460 million in AUM, showcasing institutional trust as well as a strong product-market fit, JPMorgan’s Kinexys platform continues to build out the rails for tokenised private credit, onboarding new banking partners and growing day-by-day. These examples showcase the institutional adoption of such assets, and the growing infrastructure being built in support of them. Regulatory clarity also moved forward in certain jurisdictions. Switzerland and Singapore led the charge with frameworks that treat tokenised RWAs as digitally native, legally enforceable claims, assisting in bringing institutional allocators into the ecosystem.

Total Value of On-Chain Tokenised RWAs: $23.1 billion (+22.15% over 90 days)

Regulatory, Policy & Adoption Updates:

Regulatory momentum continues to shape the global digital asset landscape, with lawmakers, central banks, and government institutions defining clearer frameworks for the industry, and thus improving legitimacy:

U.S. Updates:

- GENIUS Act becomes U.S. law (June 14): The Senate approved the “Guaranteed Electronic Notes, Issuers & Unitary Stablecoins (GENIUS) Act”, creating the first federal charter for payment-stablecoin issuers (both banks/non-banks), imposing 1-to-1 reserve, audit and AML/KYC requirements and capping interest-bearing products. The bill’s passage is widely seen as the clearest green-light Washington has given the sector to date - an extremely positive development for the world of digital assets.

- US Bipartisan CLARITY Act Introduced: On May 29, Republican French Hill introduced the Digital Asset Market Clarity Act of 2025, receiving support by members across both parties. The bill mandates disclosures on project operations and stricter asset segregation, while also outlining oversight responsibilities between the SEC and CFTC.

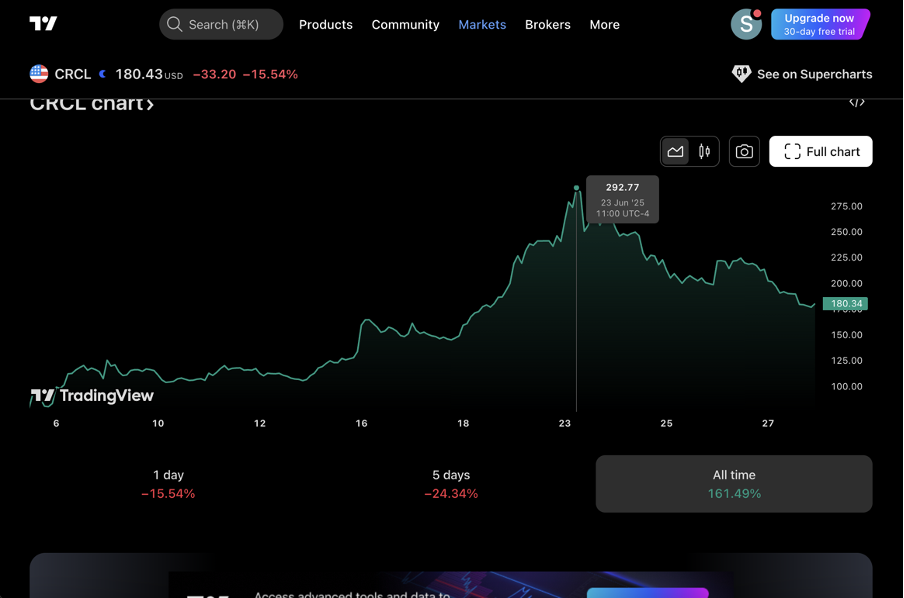

- Circle(USDC) IPO: CRCL listed on NYSE 11 June at $65and closed the quarter slightly over $180, with lead underwriters of JPMorgan, Citigroup, and Goldman Sachs.

- Coinbase expands U.S. derivatives: The exchange secured CFTC sign-off to launch perpetual-style futures for retail Americans on 21 July, filling along-standing gap in regulated domestic leverage products.

EU & UK Updates:

- MiCA Part 1 goes live: The Markets in Crypto-Assets (MiCA) regulation officially came into effect across the EU, requiring stablecoin issuers to maintain 1:1 reserves, submit white papers, and adhere to daily disclosures. Non-euro pegged coins are capped in payment utility. Part 2 (governing exchanges and token issuers) is set to activate in December.

- Coinbase obtains MiCA CASP profile in Ireland: Coinbase obtained its Crypto Asset Service Provider (CASP) license in Ireland, allowing it to legally serve all 27 EU countries under MiCA’s framework. This gives Coinbase full access to the European crypto market from its Dublin HQ.

- Kraken licensed in the Netherlands / Krak: Kraken, in anticipation of MiCA's full implementation, has secured regulatory approval as a CASP from the Dutch Central Bank, establishing itself as one of the most compliant exchanges within the European bloc. Furthermore, Kraken has launched 'Krak', a global application designed for cross-border payments and crypto asset management, enabling users to efficiently send, receive, and manage digital assets across various jurisdictions.

- ReformUK embraces Bitcoin donations: At Bitcoin 2025, Nigel Farage explained that Reform UK will accept BTC contributions and table a Crypto Assets & Digital Finance Bill cutting Capital gains taxes on digital assets to 10%, while also proposing a Bitcoin reserve at the Bank of England.

- Robinhood expands into Europe with tokenised equities & derivatives: The broker announced 24/5 trading of tokenised U.S. stocks & ETFs for customers in 30 EEA countries, introducing up to 3x crypto perpetual futures for eligible users, while also providing a proprietary Layer 2 designed for the on-chain settlement of real-world assets.

Corporate Treasury & Institutional Adoption:

After years of Strategy, formerly Microstrategy, leading the charge in allocating corporate treasuries to Bitcoin, this quarter marked a notable shift in momentum. An increasing number of public firms are following suit with consistent, strategic allocations, reflecting a maturing shift towards digital reserves. While the majority of purchases are not yet up to speed with Strategy, the growing number of firms now beginning to HODL crypto as a reserve asset is promising and supports the idea that digital assets are one’s to have as part of the balance sheet. Here are the biggest movements from Q2:

- Strategy: $1.28B added.

- TrumpMedia & Technology Group: $2.44B raised

- Mubadala: $408.5M into BlackRock’s IBIT spot-BTC ETF.

- Metaplanet: $132.7M buy

- GameStop: $450M follow-on equity; board signals proceeds for BTC accumulation.

- BitcoinTreasury Corp: C$125M initial reserve.

- SharpLinkGaming: $1B planned ETH reserve after $425M raise.

- BitDigital: $150M equity raise to pivot from mining toward ETH staking treasury.

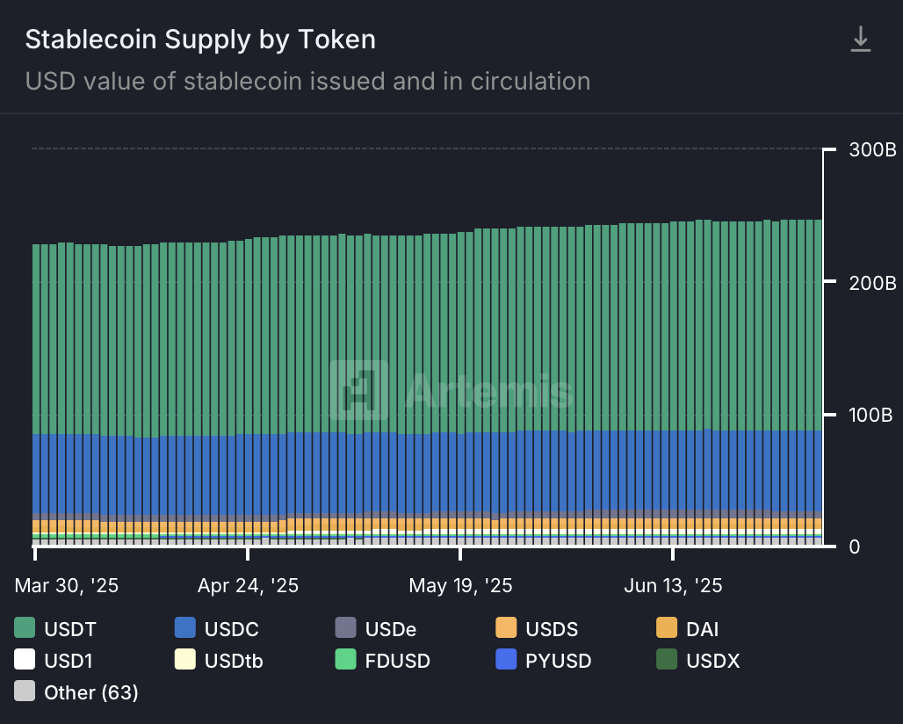

Stablecoins:

Stablecoins continue to gain traction and move into the spotlight as regulatory policies evolve and institutional adoption grows. These digital assets are increasingly being incorporated into strategies by global governments, major banks, and commodity exporters, signalling a shift away from DeFi speculation toward a financial infrastructure with practical, real-world benefits. The market cap at the close of June was $240.41B, a 17.7% increase from the $204.15B on April 1, with USDT accounting for around 64.4% and USDC accounting for around 24.6%.

Momentum behind this shift accelerated greatly in June following the U.S. Senate’s passing of the GENIUSAct - the first ever comprehensive federal legislation focused solely on regulating stablecoins in the United States. With strong bipartisan support (68/30),the legislation establishes clear rules for stablecoin issuance, mandating a1:1 backing with fiat reserves, strict Anti-Money Laundering (AML) and KnowYour Customer (KYC) requirements, as well as audited transparency. The bill also limits interest-bearing stablecoins, while also defining paths for both bank and non-bank issuers. All-in-all, the GENIUS act marks an extremely positive step forward in not only stablecoins, but the entire digital asset thesis, thus establishing the most robust legal framework for digital dollars to date. The legislation was not only a win for consumer protection and financial stability, but also widely interpreted as a reinforcement of U.S.dollar hegemony in global digital infrastructure. J.D. Vance, speaking at Bitcoin2025, framed it succinctly: “We do not think that stablecoins threaten the integrity of the U.S. dollar. Quite the opposite. We view them as a force multiplier of our economic might”.

Further, more positive news came from the Initial Public Offering of Circle Internet Group (the issuer of USDC),which saw an incredible rally from an initial listing of $65.00 to an ATH of $292.77 per share on the 23rd of June - all within that month. The listing marks yet another monumental moment for stablecoins whilst also showcasing strong demand for the integration of stablecoins into public capital markets.Despite retreating to $180.34 by the end of Q2, the performance (a 161%increase from the IPO price) indicates strong institutional belief in USDC’s future, as well as Circle’s ability to scale compliant, dollar-backed liquidity channels. With underwriting led by JPMorgan, Citigroup and Goldman Sachs, and large interest from top institutions such as BlackRock and ARK invest, the IPO has reinforced the view that stablecoins are transitioning from a fintech fairytale to a key bridge between TradFi and DeFi.

What’s Next?

As Q3 begins, markets are emerging from the smoke and dust of a chaotic Q2 with a renewed optimism.While the previous quarter was dominated by trade wars, military conflict and restrictive monetary policy, the months ahead may offer the first signs of resolution, however they may also result in escalation. At the moment, on the macro front, all eyes are on August 1st, when the widespread tariffs hit global markets. Global sentiments across equities, rates and commodities will likely be left in the hands of the White House’s approach, alongside any potential trade agreements that are able to be made with the affected countries.Simultaneously, markets are increasingly pricing in a rate-shift later this year, with escalating tensions on Chair Powell to loosen the money supply becoming more and more apparent.

In this context, digital assets are no longer running parallel to financial markets, but are being integrated into the global system, absorbing volatility, while simultaneously redirecting capital. The passing of the GENIUS Act, this quarter’s major development, acts as a formal declaration that the United States sees programmable, fiat-backed dollars as an expansion of its monetary reach, leading the charge in regulatory clarity, and thus adoption. In addition, with Europe building its own framework through MiCA, a global stablecoin architecture is being built real-time, and with it, new rails for liquidity, cross-border transactions, and faster and cheaper rotations of capital. But the story doesn’t stop at stablecoins. This quarter has illustrated that crypto is evolving on multiple fronts at once.ETFs are anchoring institutional legitimacy and providing consistent inflow mechanisms across BTC, ETH, and soon SOL. Tokenised RWAs are drawing in real-world liquidity, with the likes of BlackRock, JPMorgan, and major sovereign players building on-chain rails to re-platform legacy assets. As well as this, Bitcoin’s performance in the face of macro chaos, from tariffs to war, has begun to reposition it not just as digital gold, but as a sovereign-scale hedge against systemic volatility.

All in all, these developments mark a turning point. Digital assets didn’t just survive an extremely turbulent quarter, they held firm, absorbed volatility, and in many cases, advanced. As we enter Q3, the groundwork laid during a chaotic Q2 positions the space for amore constructive second half of 2025. With regulatory clarity accelerating, infrastructure maturing, and capital returning, the path forward looks increasingly aligned with integration, adoption, and upside. If Q2 was the stress test, Q3 may be the breakout.

Lighthouse Capital is the trading name of Lighthouse Collective Capital Fund Ltd.