Q2 2024

A Steady Light Through Stormy Seas

Dear Investors and Colleagues,

Welcome to the Q2 2024 edition of Perspectives from the Lighthouse, our quarterly newsletter. In this issue, we delve into our fund's performance amidst a volatile market landscape, explore the latest developments in the crypto and equities markets, and share our perspectives on the coming quarter.

Q2 Macro overview: A Volatile Quarter

Our strategic emphasis on pair trades mitigates our exposure to overall market volatility, distinguishing us from our liquid crypto fund peers. It is important to differentiate between general market volatility and the volatility between individual cryptocurrencies. The latter is a vital component driving returns for our strategy.

During Q2 2024, the market's focus shifted from the crypto-specific narratives prevalent in Q1 to macroeconomic and geopolitical factors, leading to higher-than-average correlations within the sector. Despite this, we executed 27 pair trades in the quarter, achieving an average return of +11% and a win rate of 65%; however, performance in the second quarter was adversely impacted by maintaining positive net directional exposure, which varied throughout the period.

Below is BTC’s 1-Day chart for the March - June period. The price ranged from $57K to $72K (a 26% range) and saw one-and-a-half round trips between these levels in three months. Major price movements aligned with key events highlighted below, underscoring the market’s sensitivity to non-crypto related data points.

April 1st: Israel initiates airstrikes on Iranian-affiliated targets in Syria.

April 12th: Onset of cryptocurrency market downturn following higher-than-expected inflation expectations.

April 13th: Acceleration of cryptocurrency market decline, coinciding with Iran's retaliation against Israel.

May 1st: Cryptocurrency market bottoms. The Federal Reserve strikes a more dovish tone, announcing a larger-than-anticipated reduction in quantitative tightening and emphasizing unemployment in its mandate.

May 3rd: Significant market rally driven by weaker-than-expected April unemployment data, marking the weakest jobs report in six months, with unemployment rising by 10 basis points to 3.9%.

May 10th: Market selloff to $60.4K prompted by Michigan inflation expectations of 3.5% for one year and a 10 basis point increase to 3.1% for five years.

May 15th: Significant rally following a slightly positive Consumer Price Index (CPI) report.

May 20th: Significant rally fueled by rumors of the SEC's approval of an Ethereum Spot ETF.

June 7th: Beginning of a decline in Bitcoin, influenced by a hawkish Federal Open Market Committee (FOMC) dot plot.

June 24th: Bitcoin experiences a sharp drop as Mt. Gox announces in-kind distributions of 140K BTC starting in July.

July 4th: Announcement of significant Mt. Gox BTC distributions commencing, alongside elevated German government sales.

While global liquidity has traditionally correlated well with crypto markets, the current heightened sensitivity to minor macroeconomic data reports is novel. We anticipate a more constructive environment for crypto in the second half of 2024, extending into 2025.

Q3 Forecast: Positive on the crypto majors, neutral on altcoins

We maintain a favorable outlook on the near and medium-term potential of Bitcoin (BTC) and Ethereum (ETH), supported by the following considerations:

- Ethereum Spot ETFs Launch and Market Outlook: On July 23rd, Ethereum (ETH) Spot ETFs are set to launch. For an in-depth analysis of the positive implications of this event, please refer to the section titled "Bitcoin vs Ethereum Narrative" below.

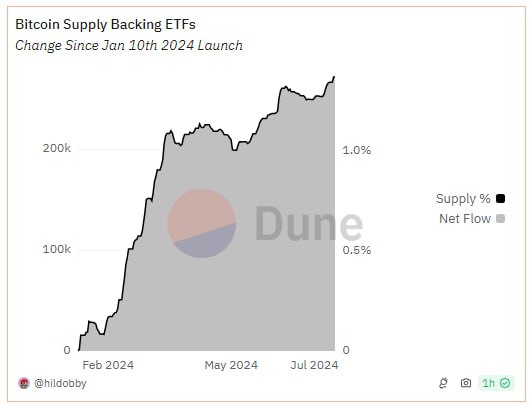

- Bitcoin ETF Holdings and Market Sentiment: In Q2, net new spot Bitcoin (BTC) ETF holdings increased by 10-15%. We anticipate this upward trajectory to persist in the second half of 2024, as discussed in our Q1 Quarterly Report. Notably, during a CNBC interview on July 15th, Blackrock CEO Larry Fink endorsed Bitcoin as "a legitimate financial instrument" that "everyone should hold." Blackrock oversees $10 trillion in client assets.

- Federal Reserve Policies and Economic Indicators: Historically, Bitcoin has correlated positively with the Federal Reserve's interest rate cuts and potential increases in global liquidity. Recent economic and corporate earnings data indicate weaker-than-expected inflation and unemployment rates following somewhat elevated readings in Q1, alongside broader economic cooling. While it is premature to forecast 2025, we currently anticipate that the Federal Reserve may resume monetizing US Treasuries once the Treasury Department’s account surplus is exhausted later this year.

- Political and Regulatory Landscape for Cryptocurrency: This election year has ushered in a more favorable political and regulatory environment for cryptocurrencies. The leading US Presidential candidate, Donald Trump, has expressed support for the crypto industry. At a minimum, a Trump administration is expected to exert less regulatory pressure, particularly benefiting entities currently under scrutiny, such as Uniswap and Lido DAO, which are facing SEC enforcement actions.

- Bitcoin Halving Impact: The beneficial effects of the Bitcoin halving are still forthcoming. In our Q1 Quarterly Report, we noted that the halving's immediate impact might be less significant than many market participants anticipated. Historically, new highs are achieved 6-9 months post-halving, aligning with the period of Q4 2024 to Q1 2025. The halving typically results in challenging conditions for miners, leading to forced selling and a market shakeout. As this subsides, the reduced supply rate becomes a more dominant market driver. Observing large publicly traded Bitcoin miners, who are currently better capitalized than during the last halving, suggests that miner selling is ongoing. However, data from Coinglass indicates that many smaller miners have recently shifted from net sellers to a more neutral stance.

While we maintain a constructive top-down outlook, our bottom-up assessment of the cryptocurrency sector is more tempered, ranging from neutral to bearish. In the absence of substantial sales and earnings, capital flows are the primary drivers of market entry. Currently, these flows are predominantly channeled through venture capital investments and exchange-traded funds, which support pre-token and early-stage projects, as well as leading cryptocurrencies.

The upcoming launch of Ethereum (ETH) ETFs is anticipated to be a positive catalyst for the market, particularly benefiting the Ethereum ecosystem. However, significant new inflows into the broader altcoin market may necessitate the advent of groundbreaking innovations and applications. Historical precedents include the rise of decentralized finance (DeFi) in 2021 and initial coin offerings (ICOs) in 2017. Such innovations must be evidently transformative to attract incremental capital from non-crypto participants, thereby bolstering altcoin valuations.

While we anticipate that altcoins may experience short-term gains alongside major cryptocurrencies and potentially outperform in the near term, their medium-term performance may remain subdued on a relative basis. This is particularly true for altcoins with higher token dilution, which have historically underperformed during extended periods, a trend observed throughout 2022 and most of 2023.

Ethereum vs Bitcoin Setup

We are positive on Ethereum versus Bitcoin heading into Q3. The launch of Ethereum's spot ETF on July 23rd should drive incremental capital flows. Market sentiment is negative, however, with many market participants expecting limited institutional interest and significant sell pressure from Grayscale Ethereum Trust (ETHE) holders. We believe the prevailing concerns are unfounded with the latter driven by recency bias following initial Grayscale BTC spot ETF selling.

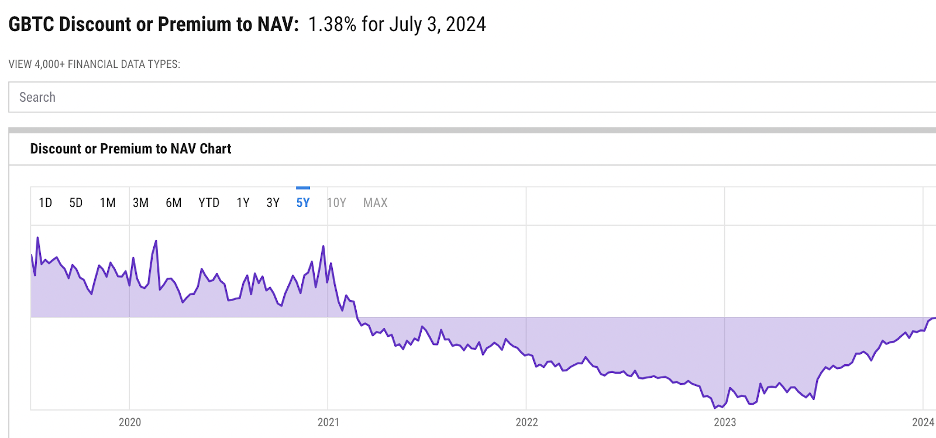

The notion that ETHE holders will be net sellers is rooted in recency bias and lacks data support, reflecting a misunderstanding of ETHE's mechanics. Proponents of this view draw parallels with the substantial selling observed when Grayscale's Bitcoin Trust (GBTC) was converted to an ETF in January. However, the dynamics of GBTC were markedly different from those of ETHE.

The first opportunity for GBTC holders to exit without significant penalties since February 2021 arose with the launch of BTC spot ETFs. GBTC had been trading at a discount to its Net Asset Value (NAV) since February 2021, with the discount reaching up to 49% in January 2023 and remaining above 43% until June 2023. The discount began to narrow as arbitragers and speculators bet on BTC spot ETF approval. On January 9, 2024, two days before conversion, GBTC still traded at a 7% discount to NAV, which narrowed to 2% on January 10.

Many speculators purchased GBTC in the fall of 2023 specifically to arbitrage the discount between GBTC and BTC. This, combined with the sell pressure from investors who had been held captive in GBTC due to its persistent discount to NAV for nearly three years, contributed to the selling pressure upon conversion.

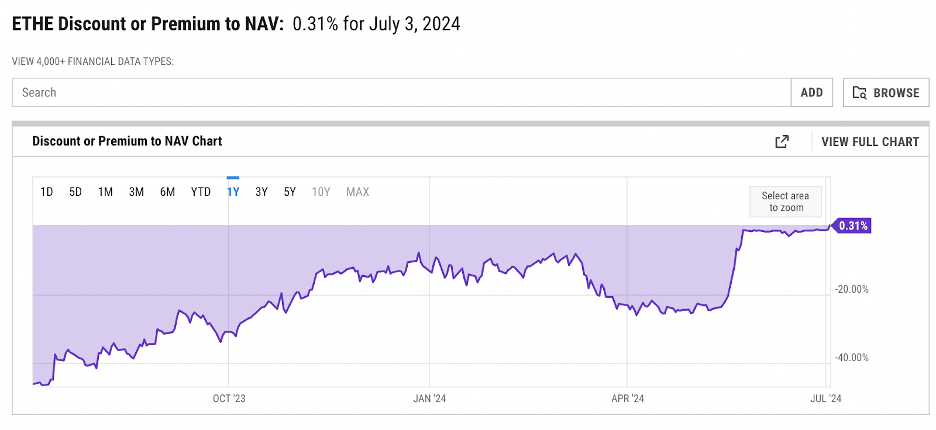

Conversely, ETHE has traded in line with NAV since May 24, 2024. Upon ETF launch, it will have traded in line for almost two months. This crucial detail is often overlooked by most crypto commentators, many of whom are unaware that ETHE is a liquid fund.

ETHE's average daily trading volume stands at approximately $90 million, representing around 1% of its Assets Under Management (AUM). The bid/ask spreads are tight, with more than $20 million of liquidity available within 0.1% of the price. This liquidity and tight spread indicate a healthy market for ETHE, which should help mitigate potential volatility around the ETF launch.

On July 3, 2024, ETHE traded at a premium to its Net Asset Value (NAV), indicating potentially higher relative institutional interest compared to Bitcoin (BTC). It is noteworthy that despite Grayscale Bitcoin Trust (GBTC) trading at a discount until the launch day of spot BTC ETFs, these ETFs have subsequently garnered over $16 billion in net inflows.

Recent reports from Blackrock and Bitwise highlight that a significant number of investors have acquired BTC ETFs as a proxy for betting on blockchain adoption. While BTC primarily serves as a digital store of value and a speculative financial vehicle, Ethereum (ETH) is utilized for conducting transactions on the blockchain, positioning it as a more direct play on blockchain adoption. It is plausible that a segment of BTC investors will either transition from BTC to ETH ETFs or add ETH alongside their BTC holdings.

Institutional adoption of Ethereum has significantly accelerated from late 2023 into 2024, highlighted by several major developments. Coinbase launched its blockchain, Base, which settles onto Ethereum, enhancing its transaction and settlement capabilities. Blackrock introduced a money-market fund on the Ethereum blockchain, furthering its utility in financial markets. Additionally, several large banks and governments have piloted bond issuance on Ethereum, demonstrating its viability for large-scale financial applications. Major corporations such as InBev, Unilever, Deloitte, and Ernst & Young are also exploring Ethereum for supply chain, tax, and audit projects. These advancements underscore Ethereum's position as the leading proxy for expanding blockchain use.

On the supply side, there is over $20 billion worth of Bitcoin (BTC) held by Mt. Gox creditors and the U.S. government, accounting for 2% of BTC’s total market capitalization. Notably, 64% of Mt. Gox creditors opted for a 10% haircut on distributions for early access to BTC, suggesting that at least 64% are likely near-term sellers, with distributions commencing between July 23-30th. In contrast, the amount of Ethereum (ETH) available for purchase on exchanges is at multi-year lows, potentially exacerbating any demand shocks.

BTC experiences consistent sell pressure from its network operators due to its Proof-of-Work consensus mechanism, which adjusts computational complexity based on the collective hash rate. Since its launch, the BTC network has seen a significant increase in its hashrate, up more than 5x since 2021. This growth is driven by miners investing tens of billions of dollars in high-performance data centers to compete for network rewards. Consequently, the BTC mined (approximately $10 billion annually) is largely sold to cover operating expenses. In contrast, Ethereum uses a Proof-of-Stake consensus algorithm that is less computationally intensive, with roughly 28% of its supply staked, effectively removing it from the supply pool.

BTC’s current annual inflation rate is 0.8%, double that of ETH’s 0.4%, averaged over the past 30 days. Ethereum’s inflation rate fluctuates with network usage and can become negative. Recent data indicate increasing usage among Ethereum Layer-2 networks, particularly optimistic rollups, driven by Arbitrum and Coinbase’s Base network.

In addition to Ethereum’s superior supply and demand dynamics relative to Bitcoin, it is also trading near its lows of the past three years on a relative basis.

The Regulatory Environment is Improving

The regulatory and political environment for cryptocurrencies in the United States saw notable improvements in Q2. The passage of the Financial Innovation and Technology for the 21st Century Act (FIT21) by the U.S. House of Representatives marked a significant step forward. This bill aims to provide clear regulations for digital asset markets, designating the Commodity Futures Trading Commission (CFTC) as the primary regulator for digital commodities while the Securities and Exchange Commission (SEC) retains authority over securities. The bill garnered bipartisan support, with 71 Democrats and 208 Republicans voting in favor, despite opposition from the SEC and the Biden administration, which criticized the bill for potentially creating regulatory gaps and risks to market stability.

In addition to FIT21, the SEC approved Ethereum (ETH) spot ETFs in May, which are expected to launch in the second half of July. This about-face represents a shift towards a more accommodating regulatory approach, potentially leading to significant inflows into these investment products.

The departures of notable crypto hawks from key positions have also contributed to a more favorable regulatory landscape. The exit of Jelena McWilliams as head of the Federal Deposit Insurance Corporation (FDIC) and Valerie Szczepanik as head of the SEC’s Digital Assets Division has removed some of the staunchest critics of the crypto industry from influential roles. Christy Goldsmith Romero is Biden’s nominee for FDIC chair. She has suggested that banks should be allowed to provide services to digital asset companies, a stance that contrasts with current restrictions and pressures faced by the crypto industry from bank regulators.

Furthermore, the financial political landscape regarding cryptocurrency has evolved, with increasing support for pro-crypto political action committees (PACs). The Fairshake Super PAC, along with its affiliates, has raised $78 million to support crypto-friendly candidates in the 2024 elections. Additionally, Coinbase-backed efforts have contributed $85 million to political activities aimed at promoting cryptocurrency interests. In the house, Republicans have 238 pro-crypto candidates and Democrats have 68. Democrats have 38 anti-crypto politicians with Republicans at just 5. In the senate, there are 37 strongly pro-crypto republicans and 6 pro crypto democrats, with just 2 and 10 strongly against, respectively, according to data from the non-profit advocacy group Stand With Crypto.

An improving political landscape, and the potential for a constructive regulatory approach would likely have an impact on flows, liquidity, and venture capital funding into 2025 and beyond.

Closing Remarks

As we enter the second half of 2024, we are proud to reflect on the achievements of the past quarter. Despite navigating through market turbulence, our fund has demonstrated resilience, positioning us strategically for future opportunities in both crypto and equities markets. The continuous refinement of our systems and operations enhances our ability to capitalize on market dislocations and deliver sustainable returns to our investors.

We extend our gratitude to our investors and partners for their support in this nascent and critical stage. Transparency remains at the core of our approach, and we are committed to keeping you informed about our strategies and performance. Please don’t hesitate to reach out for further discussions—we value your insights and feedback as we navigate this journey towards long-term growth and success together.

Lighthouse Capital is the trading name of Lighthouse Collective Capital Fund Ltd.