Q1 2026

The Signal Through the Static

As we set our compass toward 2026, the “Lighthouse” metaphor matters for a different reason than it did in the prior cycle. In a market once dominated by linear adoption narratives and directional beta, 2025 forced a more sober reality: digital assets are now fully embedded in the global macro and geopolitical transmission mechanism. When geopolitics destabilizes liquidity and risk appetite, crypto does not sit outside that system—it amplifies it.

This letter serves three purposes: (i) a deep-dive retrospective of a historic year, (ii) a granular analysis of the geopolitical “great testing” we face in 2026, and (iii) a transparent update on our evolution into a robust institutional platform. Rough seas still remain. We do not predict the waves; but we aspire to weather them.

Features that defined 2025

- The market regime shifted on October 10, 2025. Liquidity dried up, correlations broke, and many legacy models became obsolete with many pre-2025 models stopped behaving as expected.

- Policy shocks became liquidity shocks. Trade policy and kinetic conflict repeatedly forced global investors into risk-off positioning—compressing liquidity precisely where digital assets are structurally most fragile.

- There was a shift away from our directional mandates and moving toward market-neutral and delta-neutral return streams.

- Market structure still permits perverse incentives during liquidity stress, underscoring the need for credible “rules of the road.” The second half of the year reinforced what the industry learned in 2022: when liquidity thins, market power concentrates, and the incentives of vertically integrated venues (dealer + broker + clearing function under one roof) can create outcomes that look less like price discovery and more like extraction by large players.

- Regulatory market structure is the single most important catalyst for institutional participation. The CLARITY Act (and the politics around it) is the area we are watching most closely, because “rules of the road” are what unlock broad participation—and what constrain the worst consumer harms that appear when liquidity breaks.

Strategic pivot: resilience over narrative

Our positioning entering 2026 is therefore not built around long-horizon narrative bets. Lighthouse is a multi-strategy platform with a core sensitivity to liquidity conditions, flows, and the demand function for the asset class. We remain constructive on the long-run utility of blockchain-based financial rails, but our edge is not predicting “which story wins.” Our edge is maintaining a platform that performs under all market regimes. We may not outperform across all market conditions, but we cap the downside risk.

Firm Update:

Platform evolution: from a set of strategies to a resilient system

We aim to allocate not to any single macro or crypto narrative, but to compound across market regimes by allocating to strategies that can remain defensible when correlations break and liquidity thins.

Expansion of strategies

- We launched our multi-strategy program for BTC investors in May with the same strategies as our USD shareclass

- We grew the firm from with 6 strategies in Q1 and closed the year with 16 strategies.

- In 2026 we’ll scale scale thoughtfully toward ~20 strategies across our three core mandates (Market Neutral, Directional, Delta Neutral)

Allocation breakdown: resilience by design

Our portfolio construction reflects a simple view: in digital assets, volatility is normal, but liquidity discontinuity is existential. We therefore bias toward strategies that can harvest dispersion, funding, and microstructure inefficiencies without requiring a strong directional tape.

Risk Posture: Leverage is a tool, not a thesis

In 2025 our leverage at the fund level ranged between 1.5x to 2.2x as we came up against our fixed 30% of AUM concentration limits per strategy. In 2026 we will target leverage up to ~3x at the fund level primarily by adding 4 market-neutral strategies which will improve capital efficiency and allow us to make use of unused leverage through added diversification.

Manager selection and pruning:

Our 2025 experience mirrored a broader industry reality: managers that performed well in 2024 and years prior did not necessarily perform well in 2025. The regime changed faster than many models could adapt. Managers who performed in 2025 were those who continuously refreshed their models and optimized for a changing market structure.

- 2025 manager turnover: 22%. This is in line with Crypto hedge fund industry expectations. (N.B tradfi turnover rates are approximately 15-20%)

- 2026 expected turnover: ~25%.

- Importantly, our highest turnover in 2025 was in directional strategies—not because “directional can’t work,” but because many directional models trained in prior regimes stopped functioning when the rules changed (policy shocks, correlation breaks, liquidity collapse).

- This aligns with what we heard across our ecosystem: managers that looked strong in 2024 and earlier did not necessarily perform well in 2025; managers that performed in 2025 were those who constantly re-optimized and refreshed their process as the market changed.

Talent and governance:

We expanded the team in 2025, including hiring a quant researcher & analyst, a Head of talent acquisition to facilitate the hiring of new managers and a CFO to deepen diligence, accelerate sourcing in a capacity-constrained opportunity set and support operations and financial oversight.

Updates for 2026

Based on our learnings from 2025, we are formalizing the following implementation priorities below:

2025 Market Retrospective: Anatomy of the Reset

To understand our positioning for 2026, we’ll look back to 2025. It was a year bifurcated by a dramatic shift from macro-political shock in the first half to structural market failure in the second. The lesson is simple: in an environment defined by persistent geopolitical fracture, liquidity is the dominant state variable.

H1 2025: The Geopolitical Stranglehold

The first half of 2025 was dominated by uncertainty. Capital flows were dictated less by protocol fundamentals and more by the capricious winds of trade wars and kinetic conflict. When the world reprices risk, crypto does not sit outside the system - it amplifies it.

The “Liberation Day” trade shock (April)

The volatility began with a sharp escalation in U.S. trade policy, including the April 2, 2025 executive order establishing a reciprocal tariff regime (Executive Order 14257). In markets, the near-term mechanism was familiar: risk-off positioning compressed liquidity and temporarily raised correlations across asset classes, challenging the “uncorrelated asset” thesis held by many allocators.

- Market reaction: correlations spiked and liquidity thinned across higher-beta crypto assets.

- Second-order effect: supply-chain uncertainty damaged confidence even as markets attempted tactical rebounds.

Portfolio implication: dispersion widened between high-quality, liquid majors and long-tail altcoin liquidity. For digital assets, the relevance is not the tariff itself—it is the mechanism:

- Risk-off flows compress liquidity,

- correlations rise when investors de-risk indiscriminately,

- Crypto - given how much thinner trading is across many crypto assets compared to TradFi, liquidity shocks are felt much more keenly.

This is one of the most important reasons we bias toward market-neutral and relative-value: we do not need to be “right” about the direction of the macro headline to monetize dispersion and dislocation.

H2 2025: The “Apathy Peak” and the Great Flush

The second half of the year brought improving regulatory clarity masked by speculative reflexivity that ultimately required a painful correction. As always, leverage is invisible when liquidity is abundant and obvious when the bid disappears.

The Digital Asset Treasury (“DAT”) bubble

Following major legislative developments on stablecoins in 2025, parts of the equity and corporate treasury ecosystem attempted to front-run a new institutional era. Certain public vehicles and corporate “digital asset treasury” strategies traded at sustained premiums to underlying holdings, creating a reflexive feedback loop that inflated risk-taking and crowded positioning.

- The trap: investors mistook financial engineering for organic demand.

- The tell: retail participation remained muted even as leverage pockets grew.

- The consequence: a thin, leverage-supported tape became vulnerable to a liquidity cliff.

October 10: the deleveraging shock and regime change

Within our internal framework, October 10, 2025 was not “just another sell-off.” It was a market-structure-changing event. Liquidity dried up, correlations broke, and every model trained on the abundant-liquidity world became suspect. The market has been searching for a new equilibrium since.

Our observation since October 10 is direct: when liquidity evaporates, well-funded players can step in to dominate price formation. This remains endemic to crypto because in too many places the dealer, the broker, and the clearing function are effectively intertwined. The resulting incentives can look less like price discovery and more like extraction - the same structural weakness the industry confronted from the FTX collapse.

2026 Strategic Outlook: The Geopolitical Crucible

The Core Red Flags We’re Monitoring

- Sustained rise in real yields and the term premium: when the market starts demanding more compensation to hold duration, capital becomes more selective. Crypto’s “optionality” premium compresses.

- Safe-haven bid migrating from the USD to gold/silver: this is a regime signal. It implies credibility or fiscal anxiety, which can keep rates elevated and risk appetite fragile.

- A “sell the USA” narrative: rising yields alongside a softer USD is the worst of both worlds for risk assets—tight financial conditions plus currency uncertainty.

- Liquidity bifurcation: BTC/ETH remain tradable; alts lose bid depth. That’s when manipulation risk rises and market structure flaws become most visible.

- Sanctions/payment shocks: stablecoin settlement grows, but risk premia rise and on/off-ramp friction increases.

The takeaway for crypto markets: in the short run, higher yields and risk-off positioning make crypto less interesting as a marginal allocation; in the medium run, instability increases demand for crypto rails (stablecoins), while creating frequent volatility regimes that reward tactical and market-neutral trading.

We are watching two primary vectors.

The recent Greenland dispute may have burned itself out after the recent Davos conference, but Trump’s affection for dramatic tariff increases on both allies and rivals is here to stay. Market reactions to tariff surprises are driving risk-off behavior and safe-haven flows (gold/silver up) alongside pressure on risk assets, including bitcoin.

Why this matters: the domino chain that leads into crypto

Domino 1: Tariff threats on allies → transatlantic trust premium break

- When tariffs are threatened against close allies over a sovereignty dispute, markets stop treating this as a negotiable trade spat and start treating it as a structural rupture risk in the post-2025 order.

Domino 2: Retaliation cycle risk → growth uncertainty + inflation uncertainty rises

- Tariff escalation is uniquely toxic because it can create simultaneous growth drag and price pressure (a stagflationary impulse), which increases uncertainty in the inflation path and rates path.

Domino 3: Rates volatility and term premium → “sell USA” conditions become plausible

- The discussion isn’t only about retaliatory tariffs. There is also market chatter about Europe’s financial leverage (including the idea—credible or not—that Europe could reduce demand for U.S. assets). U.S. officials have publicly pushed back on this “sell Treasuries” narrative, but the fact that it’s being discussed at all is the signal: markets are stress-testing capital account politics, not just trade policy.

Domino 4: Safe-haven rotation → gold/silver lead, risk assets de-rate

- As the uncertainty premium rises, investors rotate toward safe havens. In recent market coverage of the Greenland-tariff episode, safe-haven moves (gold/silver strength) coincided with broad risk-off pressure.

- In that narrative, crypto tends to lose its marginal buyer because higher real yields + volatility in policy outcomes make “optional” risk less attractive.

Domino 5: Crypto impact is mechanical: liquidity drains, basis/funding compresses, alts break first

In a transatlantic-fracture / tariff-escalation risk-off regime, crypto typically transmits through:

- Liquidity withdrawal: spreads widen; depth disappears first in long-tail tokens.

- Funding/basis instability: carry becomes unreliable; funding flips more frequently.

- Correlation spikes: crypto trades more like a high beta liquidity instrument than a diversifier.

The most consequential macro risk for crypto in 2026 is not a single war headline; it is a credibility shock to U.S. monetary governance, because that can reprice the entire discount-rate complex.

Domino chain

1. Perceived politicization of policy → markets price a credibility risk premium.

2. Credibility premium shows up as higher rates volatility and/or a higher term premium.

3. If confidence is impaired, you can get a non-linear pattern: yields up + USD down (“sell USA”).

4. In that regime, the safe haven rotation often looks like gold and sometimes silver leading, while risk assets de-rate.

5. Crypto, in the near term, becomes less interesting:

- Carry returns become available in cash/T-bills,

- Risk budgets get reduced,

- Vol-target strategies cut exposure,

- Long-only crypto capital becomes more tactical.

Crypto-specific second/third-order effects

- BTC’s long-run “non-sovereign” appeal may strengthen conceptually, but tactically higher real yields and forced deleveraging dominate flows.

- The fragility shows up first in alts, then in perps funding, then in basis, then in options skew—the sequence matters.

- Opportunity set: correlation breaks, vol-of-vol, funding dispersion, and relative value between spot/perps/options expand materially. This is where multi-strats can thrive while narratives fail.

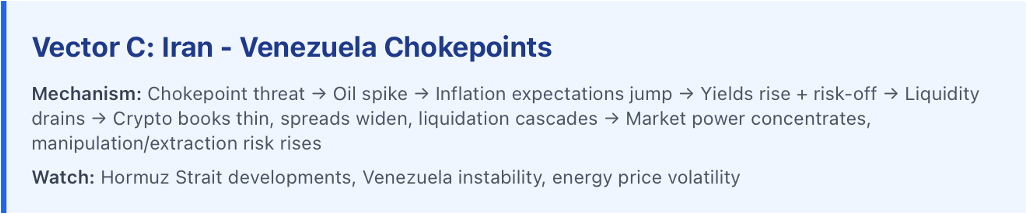

Energy chokepoint risk is the cleanest pathway from geopolitics into inflation—and from inflation into crypto drawdowns.

Domino chain

1. Any credible threat to a chokepoint → oil spike → inflation expectations jump.

2. Inflation expectations jump → yields rise → risk-off.

3. Risk-off + yields up → liquidity drains.

4. Liquidity drain → crypto books thin, spreads widen, liquidation cascades become more likely.

5. As liquidity thins, market power concentrates and manipulation/extraction risk rises—the exact structural pathology that has not been fully solved since 2022.

The Biggest Catalyst Might Not Happen: CLARITY Act

The market’s most important “rules of the road” catalyst is also the most fragile: the CLARITY Act might not pass (or may pass in a diluted/contested form).

If CLARITY advances meaningfully

- Institutional pacing improves (clearer risk/compliance posture)

- More durable liquidity enters (tighter spreads, deeper books)

- The “integrated dealer/broker/clearing” pathology begins to face enforceable constraints

- Crypto risk premium compresses over time

If CLARITY stalls or fails

- The U.S. market retains a structural risk premium: fragmented venues, uneven standards, and higher headline/enforcement volatility

- Institutional allocators slow allocations or concentrate only in the most conservative implementations (BTC/ETH, select funds, constrained wrappers)

- Long-tail assets remain structurally fragile in liquidity shocks

- The market remains prone to periodic “liquidity cliffs”—which is negative for long-only, but creates recurring dislocation opportunity for multi-strats

This is why we treat CLARITY not as a narrative, but as a market-structure hinge: it can change the quality of liquidity, not just the level.

The “Narratives” vs. “Reality”

Narratives do matter—but not as multi-year bets. Narratives matter because they shape positioning, crowding, reflexivity, and ultimately liquidity. As a multi-strategy platform trading tactically, we are not “investing in narratives.” We are trading the system that narratives distort.

The death of the “Four-Year Cycle” as a portfolio anchor

The “four-year cycle” remains a useful cultural frame, but 2025 further demonstrated that macro and liquidity dominate in an institutionalizing market. When trade policy, conflict escalation, and central bank credibility become primary drivers, the cycle is no longer sufficient as a timing model.

Our 2026 adjustment is therefore explicit:

- less dependence on cycle-timed directional exposure,

- more emphasis on strategies that monetize dispersion and microstructure,

- tighter liquidity risk constraints for any strategy that expresses beta.

The Grand Compromise: The Clarity Act and regulation as the catalyst for real participation

CLARITY Act: where things stand now, and why Coinbase’s pushback matters

This is the single most important regulatory development we are watching because it addresses market structure—the “rules of the road” for institutional adoption.

Where things stand (as of mid-January 2026):

- The House version of the Digital Asset Market Clarity Act of 2025 (H.R. 3633) passed the House and was received in the Senate on September 18, 2025 and referred to Senate Banking.

- The CRS summary on Congress.gov describes the bill as establishing a framework for “digital commodities,” generally placing transaction regulation under the CFTC, including digital commodity exchanges, brokers, and dealers.

- The Trump White House issued a Statement of Administration Policy (July 15, 2025) supporting the bill’s goals and framing it as a “good first-step” toward “commonsense rules for digital assets.”

- On January 13, 2026, Senate Banking majority materials described the CLARITY Act as a major step toward a tailored U.S. regulatory system with investor protections and law enforcement tools, released ahead of markup.

Coinbase’s pushback—and what it may mean:

In January 2026, Coinbase publicly pulled support for the Senate CLARITY Act draft in the context of negotiations, highlighting industry friction about what the rules should be and how they impact business models. Reporting indicates this contributed to delay dynamics around the markup and surfaced substantive disagreements (including around issues like stablecoin rewards and what consumer “protections” should look like in practice).

From our perspective, Coinbase’s pushback signals three things investors should take seriously:

1. The industry is not monolithic. “Crypto wants regulation” is too simplistic. Different segments want different outcomes—banks, exchanges, DeFi, stablecoin issuers, brokers, and token projects all have conflicting incentive sets.

2. The Senate version will likely evolve materially. The Senate is where compromises get harder, and where edge cases (stablecoin yield, DeFi classification, custody standards, broker-dealer style obligations) become the real fight.

3. Timing risk is real, but direction-of-travel remains toward greater clarity. Even if the schedule slips or the language changes, the center of gravity has shifted: institutional participation requires enforceable market structure.

Why CLARITY matters to our 2026 outlook:

We are not cheering for a bill because it is “good for price.” We are focused on market integrity.

Our core observation since October 10 is that liquidity discontinuity creates the conditions where manipulation becomes easier and where consumers are most exposed—especially in an ecosystem where the dealer, broker, and quasi-clearing functions can be consolidated.

A credible market-structure regime is what enables:

- Segregation of functions and responsibilities,

- Enforceable disclosure and conduct standards,

- Auditable execution and best-execution expectations,

- Ultimately: institutional participation at scale.

That is why CLARITY is central to how we think about 2026—not as a “narrative,” but as a structural constraint on the worst behaviors that emerge when liquidity breaks.

Closing Thoughts: The Long View

The four-year cycle did not deliver the promised euphoria in 2025, but it did deliver something more valuable: a more mature, more institutionalizing asset class that is now being forced to confront its structural weaknesses. 2026 will not be a year of “easy mode” gains; it will be a year of grinding, tactical trading, and survival.

Geopolitical shocks, policy volatility, and structural market incentives will continue to shape liquidity conditions. In this environment, simply “holding” volatile assets is a different proposition than in prior cycles. This is why we have built Lighthouse into a multi-strategy platform. When the storms come - whether from Venezuela, Greenland, or the Federal Reserve - our light remains steady.

Lighthouse Capital is the trading name of Lighthouse Collective Capital Fund Ltd.